Background to ‘flip flop’ schemes

These schemes used loans between trusts to avoid tax that would have been payable by the UK resident settlor or UK resident beneficiaries when the trust disposed of an asset. The schemes generally came in two different versions:

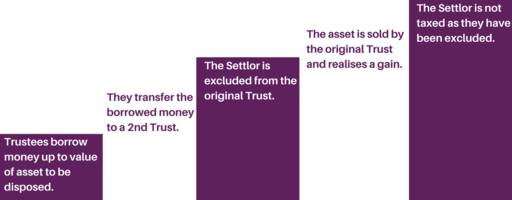

1. Avoidance of settlor interested trust provisions (s86) – A UK resident settlor who is not excluded is taxed on the gains of the trust as it arises. Steps designed to avoid s86 were:

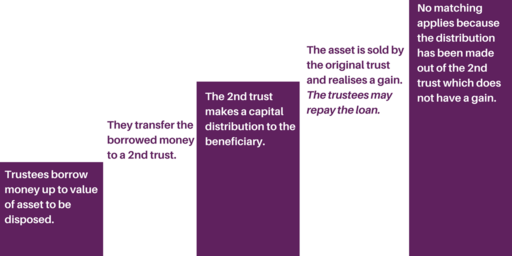

2. Avoidance of matching of gains (s87) – Gains of the trust are matched to distributions to UK resident beneficiaries which gives rise to tax payable by the recipient beneficiary. Steps designed to avoid s87 were:

Schedule 4B conditions:

- Trustee borrowing

- Proceeds of borrowing are not for ‘normal trust purposes’ – defined as payment of trust expenses, purchase of a trust asset at arms’ length, and a repayment of a loan.

- Transfer of value out of the trust (met regardless of the residence of the recipient)

The legislation is actually more wide-reaching than it needs to be to counteract the ‘flip flop’ schemes, which involved the transfer of trust property from one to another; Schedule 4B applies to any transfer of value from the Trust i.e. transfer of trust property, loan, distribution.

Implications:

Where the 3 conditions above apply, there is a deemed disposal of the chargeable assets of the trust at their market value. This does not include assets of any underlying companies, it is just the Trust’s assets.

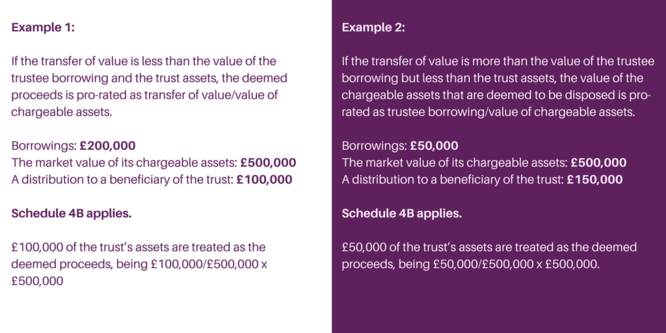

The value of chargeable assets, i.e. the deemed proceeds, is likely to be pro-rated where there are differences in the amount of trustee borrowing and transfer of value. The pro-rata calculation is also used for the base cost of the assets being disposed.

Where there is a pro-rated deemed proceeds the trust’s assets will be left with a blended base cost. If the trust is settlor-interested i.e. has a UK resident non-excluded settlor, the gain will be taxable on the settlor. If the trust is not settlor-interested, the gain must be recorded by the trustees’.

Schedule 4C conditions:

- Schedule 4B has applied and a deemed disposal has arisen.

- The transfer of value is made to a UK resident beneficiary.

- The trust is not settlor interested.

Implications:

Any gains arising on the Sch 4B deemed disposal that have not been taxed on the settlor are transferred into a stockpiled gains pool, known as the Sch 4C pool.

This pool operates in the same way as the s87 stockpiled gains pool but Schedule 4C takes priority. This means that any stockpiled gains in the s87 pool up to the date of the Sch4B transfer are ‘tipped’ into the Sch 4C pool.

Distributions to UK resident beneficiaries are ‘matched’ to the Sch 4C gains and the beneficiaries are taxed personally. Trust gains made after the Sch 4B transfer will go into the s87 pool as normal. No tax return is required for the trust and any reporting is completed through the beneficiaries’ personal tax returns. However, it is important for trustees to keep a record of the pools so they can inform the beneficiaries accordingly.