i) Introduction of taxation of gains on commercial property – URGENT ACTION MAYBE REQUIRED

Recent years have seen HMRC focus solely on the taxation of UK residential property. From April 2019 this is going to change as HMRC intends to extend non-resident capital gains tax (NR CGT) to gains on the disposal of UK commercial property. NR CGT applies to all property irrespective of how it is held (unlike ATED CGT which only applies to residential properties held by companies).

NR CGT was introduced in April 2015 for UK residential property and HMRC allowed for an uplift of the base cost of the disposed property to its April 2015 valuation. HMRC are doing the same with commercial property with a base cost uplift to the April 2019 valuation. We would therefore suggest obtaining April 2019 valuations for all UK commercial property held.

HMRC are extending the scope of NR CGT to indirect disposals of property. The disposal of shares in ‘property rich’ companies are also caught by NR CGT.

Property rich is defined as 75% or more of the gross asset value of the company being attributed to UK property. An indirect holding is defined as a person holding a 25% or greater interest in the company.

The current 20% NR CGT rate is being removed as an attempt to achieve more consistency and equality between UK and non-UK residents. Non-resident companies will be subject to corporation tax on gains whilst everyone else will be subject to capital gains tax, as is the case for UK residents currently.

The consultation document can be found here.

ii) Updated Annual Tax on Enveloped Dwellings (ATED) valuation dates

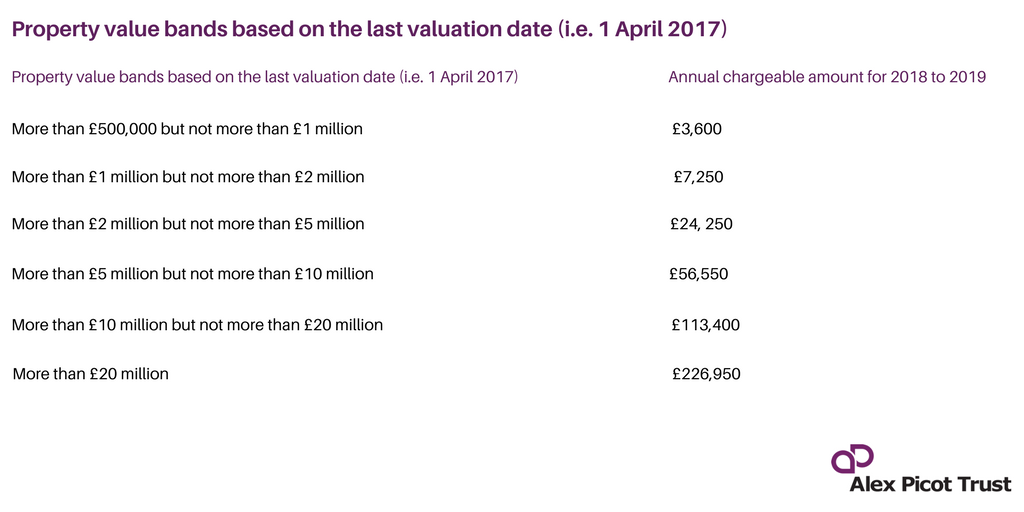

An ATED liability is determined by the valuation of a UK residential property held in a company, starting at £500,000. When ATED was introduced in April 2012, HMRC set a valuation date of 1 April 2012 as the marker to determine if properties were liable and if so which band they fell into.

The valuation date must be updated every 5 years with the first update effective for the upcoming 2018/19 ATED returns that are due before 30 April 2018. All companies that hold UK residential property with a valuation over £500,000 as at 1 April 2017 have an obligation to file an ATED return this April (2018). You do not have to obtain a professional valuation, HMRC accept valuations that have been estimated based on looking at equivalent properties provided the valuation is deemed reasonable.

It is recommended that where a property is within 10% of the ATED band threshold, a professional valuation is obtained. Alternatively, you can request a pre-return banding check from HMRC where they will confirm whether they agree with the ATED band you think the property fall into.

Where an ATED relief can be claimed, it is less important to obtain an updated valuation as the relief declaration returns do not require a valuation to be declared because there is no ATED liability. However, it may be wise to consider recording valuations, even if informal, as this is useful in the future if the property is sold or the relief ceases to apply.

The ATED bands and chargeable amounts for the 2018/19 ATED year are set out in this chart (the property valuation bands are not index-linked so we are likely to see further increases to the charges well above inflation in the future):

iii) Changes to taxation of non-resident landlord scheme

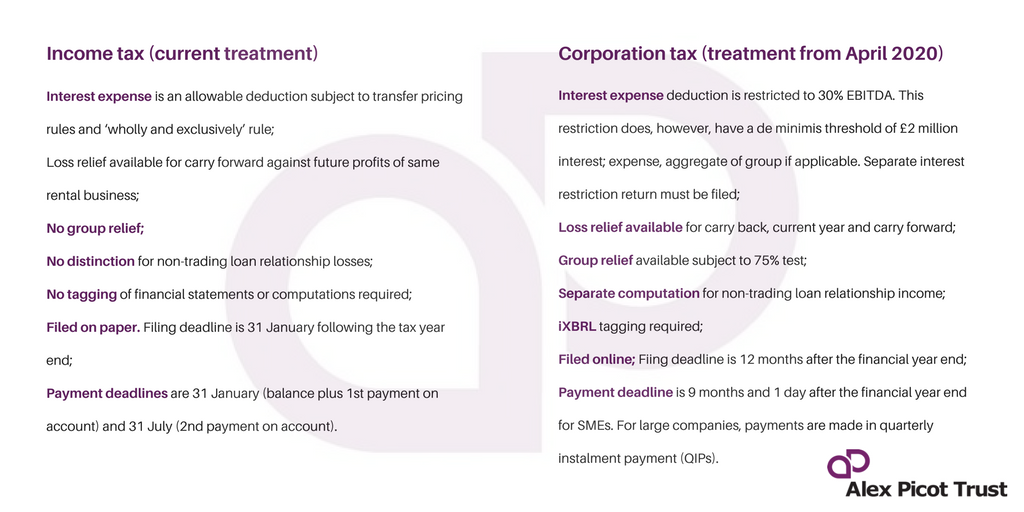

From April 2020, non-resident landlord companies will be subject to corporation tax on their UK rental income. Currently all non-resident landlords are subject to income tax on UK rental income.

At first glance, this may appear positive for non-resident companies given the reducing rates of corporation tax to 17% by April 2020. However, the corporation tax regime can be more complex.

The key differences for non-resident landlords to be aware of are:

If you’d like to speak to any of our experts about the changes that are outlined here, please contact Chris Cotillard, Director of Alex Picot Trust.